Protecting Your Home and Peace of Mind: A Senior's Guide to Home Insurance

Your home is more than just four walls and a roof—it’s your sanctuary, a place filled with memories, laughter, and years of hard work. But what if disaster strikes? A sudden storm, a burst pipe, or even an unexpected break-in could turn your safe haven into a nightmare overnight. That’s where home insurance comes in.

For many American seniors, home insurance might seem like just another bill, another complicated policy full of legal jargon. But in reality, it’s one of the most important protections you can have. The right coverage can save you from financial ruin and help you rebuild your life after an unexpected event. In this guide, we’ll walk you through why home insurance is crucial, what types of coverage you should consider, and how to make sure you’re not overpaying for your peace of mind.

Why Seniors Need Home Insurance More Than Ever

As we age, our ability to recover financially from major losses decreases. Unlike younger homeowners, who may still be in the workforce and able to earn back lost money, retirees often rely on fixed incomes. This means that a single unexpected home disaster could have devastating financial consequences.

Imagine waking up one morning to find that a tree has crashed through your roof during a storm. The damage is extensive, and repair costs could run into the tens of thousands of dollars. Without home insurance, you might be forced to dip into your retirement savings—or worse, go into debt—to cover the costs.

Even more frightening, what if someone slips and falls on your property? If they sue you, you could be looking at medical bills and legal fees that reach six figures. A good home insurance policy doesn’t just protect your house; it protects your financial future.

Understanding Home Insurance Coverage

Not all home insurance policies are created equal. It’s essential to understand what’s covered—and just as importantly, what isn’t. Here are the main types of coverage you should know about:

1. Dwelling Coverage

This covers the physical structure of your home—walls, roof, foundation—if it’s damaged by covered events like fires, storms, or vandalism. If your house is completely destroyed, dwelling coverage pays to rebuild it.

2. Personal Property Coverage

This protects your belongings inside the home, such as furniture, electronics, and clothing, in case of theft, fire, or other disasters. If a thief breaks in and steals your prized jewelry collection, this part of your policy can reimburse you.

3. Liability Protection

If someone gets injured on your property and decides to sue you, liability coverage helps pay for legal fees, medical expenses, and settlements. This is especially important for seniors who frequently have visitors, including grandkids who may be prone to accidents.

4. Additional Living Expenses (ALE) Coverage

If your home becomes uninhabitable due to a covered event, ALE helps pay for temporary housing and related expenses. Imagine your house catching fire and needing months of repairs—this coverage ensures you won’t be stuck paying out of pocket for a hotel or rental.

What’s NOT Covered?

It’s just as important to know what your policy won’t cover. Most standard policies do not include:

- Flood damage: If you live in an area prone to flooding, you’ll need separate flood insurance.

- Earthquake damage: Similar to floods, earthquakes require a separate policy.

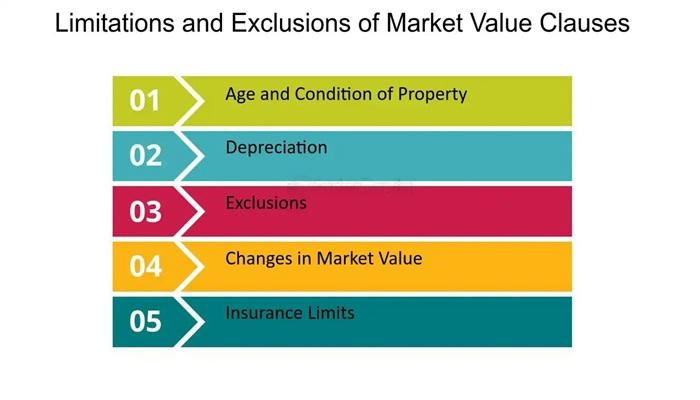

- Routine wear and tear: Insurance won’t cover old pipes that finally give out or a roof that’s simply past its lifespan.

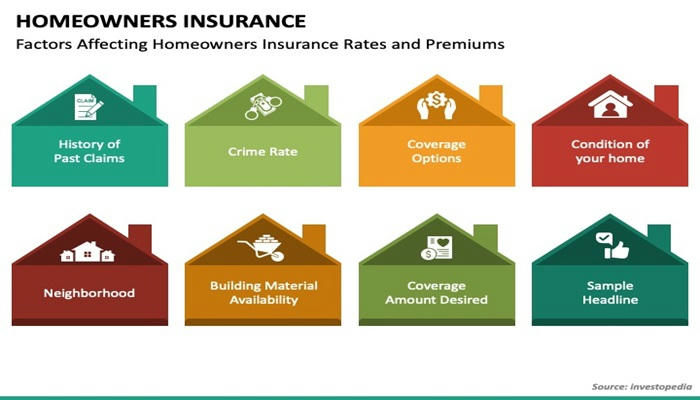

How to Save Money on Home Insurance

Many seniors worry about the cost of home insurance, but there are several ways to lower your premiums without sacrificing coverage:

1. Bundle Your Policies

If you have car insurance, check with your provider about bundling it with your home insurance. Many companies offer discounts when you purchase multiple policies from them.

2. Increase Your Deductible

A higher deductible means lower monthly premiums. If you have enough savings to cover a higher out-of-pocket expense in case of a claim, this could be a smart way to save money.

3. Improve Home Security

Installing a security system, smoke detectors, and even smart locks can lead to discounts on your policy. Insurers reward homeowners who take steps to reduce risks.

4. Ask About Senior Discounts

Some insurance companies offer special discounts for seniors. Never assume—always ask if you qualify for any age-related savings.

5. Maintain a Good Credit Score

Believe it or not, your credit score can affect your insurance rates. Paying bills on time and keeping your debt low can help you secure better rates.

The Importance of Reviewing Your Policy Regularly

Your needs change over time, and so should your insurance. Make it a habit to review your policy annually and ensure you have the right level of coverage. If you’ve recently made home improvements—like a new roof or a kitchen renovation—notify your insurer, as these updates may affect your policy.

Likewise, if you’ve paid off your mortgage, you may be able to adjust your coverage or even remove certain requirements that were initially imposed by your lender.

Final Thoughts: Don’t Gamble with Your Home

Some seniors assume they can get by without home insurance, thinking, “Nothing bad has ever happened before.” But the truth is, disasters don’t send warnings—they just happen. The last thing you want is to be caught unprepared when the unexpected strikes.

Think of home insurance as an investment in your peace of mind. It ensures that no matter what life throws your way—a fire, a storm, or an unexpected lawsuit—you’ll have the financial protection to weather the storm.

So don’t put it off. Take a look at your current policy, compare rates, and make sure you have the coverage you need. Because at the end of the day, protecting your home means protecting yourself—and the life you’ve worked so hard to build.