Preparing for Retirement: A Guide to Financial and Lifestyle Planning

Retirement is a significant milestone that requires careful planning and thoughtful decision-making. Whether you're approaching retirement age or planning well in advance, it's essential to consider both your financial security and lifestyle during retirement. By preparing early and taking proactive steps, you can ensure that your retirement years are enjoyable, fulfilling, and financially stable.

This article explores the key aspects of retirement planning, from understanding retirement savings options to preparing for a fulfilling post-work life.

1. Understanding Retirement Savings Options

The foundation of any retirement plan is a solid understanding of the savings options available. In the United States, several retirement accounts offer unique benefits:

401(k) Plans

- Contribution limits (2025): $22,500 (under age 50); $30,000 (age 50+).

- Tax benefits: Pre-tax contributions lower taxable income; growth is tax-deferred.

- Withdrawals: Penalty-free at age 59½ (taxed as income).

- Employer match: Many employers match contributions—aim to contribute enough to maximize this benefit.

IRAs: Traditional vs. Roth

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Tax Deduction | Contributions deductible | No deduction |

| Withdrawal Taxes | Taxed as income | Tax-free (if qualified) |

| 2025 Contribution | $6,500 (under 50) | $6,500 (under 50) |

Social Security & Pensions

- Social Security: Claim as early as 62 (reduced benefits) or delay up to 70 for higher payouts.

- Pensions: If available, these provide guaranteed lifetime income but are increasingly rare.

2. Creating a Retirement Budget

A realistic budget ensures your savings align with future expenses:

Key Expense Categories

- Basic Needs: Housing, utilities, groceries, transportation.

- Healthcare: Medicare premiums, prescriptions, long-term care.

- Lifestyle: Travel, hobbies, dining, entertainment.

- Emergency Fund: 3-6 months of expenses for unexpected costs.

Income Sources

- Retirement accounts: Estimate withdrawals from 401(k)/IRA (4% annual rule is a common guideline).

- Social Security: Use the SSA calculator for personalized estimates.

- Other: Rental income, part-time work, or pensions.

3. Health Care Planning

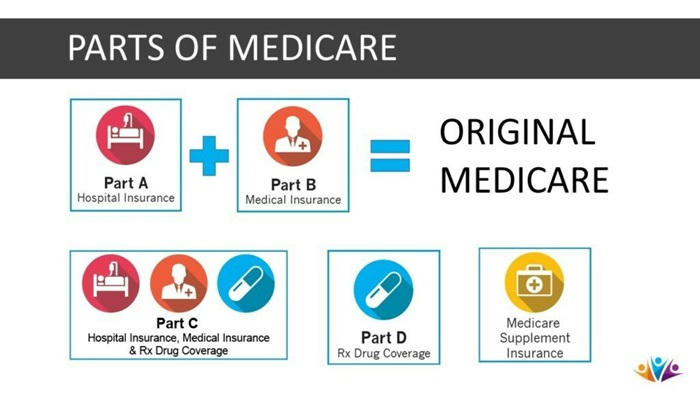

Medicare Breakdown

- Part A: Hospital insurance (usually premium-free).

- Part B: Outpatient services (~$170/month in 2025).

- Part C (Advantage): Bundled plans with extra benefits.

- Part D: Prescription coverage.

Tip: Consider Medigap or Advantage plans to cover gaps in Medicare.

Long-Term Care Insurance

- Covers nursing homes, in-home care (average cost: $100,000+ annually).

- Purchase before age 65 for better rates.

4. Housing Strategies

Options & Costs

| Choice | Pros | Cons |

|---|---|---|

| Aging in Place | Familiarity, independence | May require costly renovations |

| Downsizing | Lower expenses, simpler life | Emotional attachment to home |

| Retirement Community | Built-in support, social activities | Higher monthly fees |

5. Lifestyle & Fulfillment

Retirement isn’t just about money—it’s about joy and purpose:

Ideas to Stay Engaged

- Hobbies: Gardening, painting, photography.

- Volunteering: Mentor youth, support charities.

- Travel: Budget for trips using tools like travel rewards credit cards.

Final Thoughts

By addressing finances, healthcare, housing, and lifestyle early, you can turn retirement into a rewarding chapter. Start planning today to enjoy tomorrow’s freedom!